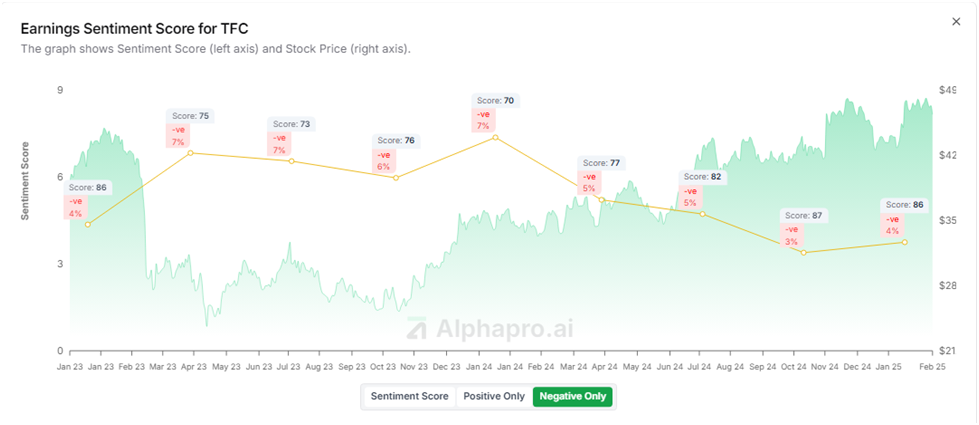

Truist Financial Corporation (NYSE: TFC) reported Q4 2024 earnings call transcripts on January 17, 2025. The results highlighted the bank’s resilience and strategic initiatives in a dynamic financial landscape, providing insights into its financial health, key growth drivers, and areas of concern.

Truist Financial Corporation’s Financial Performance Overview

Truist Financial Corporation reported net income available to common shareholders of $1.2 billion, or $0.91 per share, aligning with analysts’ expectations. The bank’s net interest income (NII) was $3.64 billion, a 0.4% decline from the previous quarter, primarily due to a slightly lower net interest margin (NIM) of 3.07%, down five basis points (bps) from Q3 2024. Total revenue also saw a 0.6% quarterly decline to $5.11 billion.

Despite this slight contraction, the bank successfully managed deposit costs, which declined by 19 bps. Truist Financial Corporation also repurchased $500 million in common shares, demonstrating a commitment to shareholder value.

Truist Financial Corporation’s Positive Highlights

Truist Financial Corporation experienced strength in investment banking and trading, with a 58.8% year-over-year increase driven by higher structured real estate income, loan syndications, and trading activity, although there was a 21.1% decline from Q3 2024. Asset quality and capital strength remained solid, as nonperforming loans decreased by 1 basis point, reflecting strong credit discipline. The Common Equity Tier 1 (CET1) ratio was 11.5%, reflecting a strong capital position. The provision for credit losses dropped by 17.7% compared to last year, showing effective risk management. Deposits also grew, with average deposits increasing by $5.7 billion (1.5%) from the previous quarter. Both interest-bearing and noninterest-bearing accounts contributed to this growth. Additionally, the cost of total deposits fell to 1.89%, a decrease of 19 basis points, which helped reduce margin pressures.

Challenges and Areas for Improvement

Revenue contraction was a concern, as total revenue declined by 0.6% quarter-over-quarter, primarily due to a 0.9% drop in noninterest income. Net interest income fell by 0.4%, impacted by lower yields on earning assets and a narrowing net interest margin. Expense management pressures persisted, with noninterest expenses rising by 3.7%, driven mainly by higher professional fees and technology investments. Adjusted noninterest expenses increased by 4.0%, reflecting continued infrastructure and risk management spending. Loan growth was also a challenge, as average commercial loans declined by 0.8%, particularly in commercial and industrial (C&I) and commercial real estate (CRE) lending, though consumer lending grew by 1.2%, led by residential mortgages and indirect auto loans.

Strategic Initiatives and Outlook

Truist Financial Corporation (NYSE: TFC) continues to focus on digital transformation with growth in digital account openings and active mobile users. The bank remains optimistic about adjusted revenue growth of 3-3.5% in 2025, supported by loan diversification, cost optimization, and capital market activities.

Final Thoughts

Truist Financial Corporation (NYSE: TFC) delivered stable earnings and strong asset quality, despite marginal revenue declines and expense pressures. The bank’s focus on digital innovation, risk management, and strategic cost-cutting positions it for long-term success.

As Truist Financial Corporation navigates 2025, investors and stakeholders will be watching loan growth trends, expense management strategies, and capital deployment initiatives to gauge its trajectory in an evolving financial landscape.